lundi 19 décembre 2016

dimanche 18 décembre 2016

mercredi 7 décembre 2016

lundi 5 décembre 2016

Why fewer companies are going public

The Bad Side of a Good Idea Why fewer companies are going public, why it’s a problem, and what we can do about it.

http://www.collaborativefund.com/uploads/Collab%20Bad%20Side%20of%20a%20Good%20Idea2.pdf

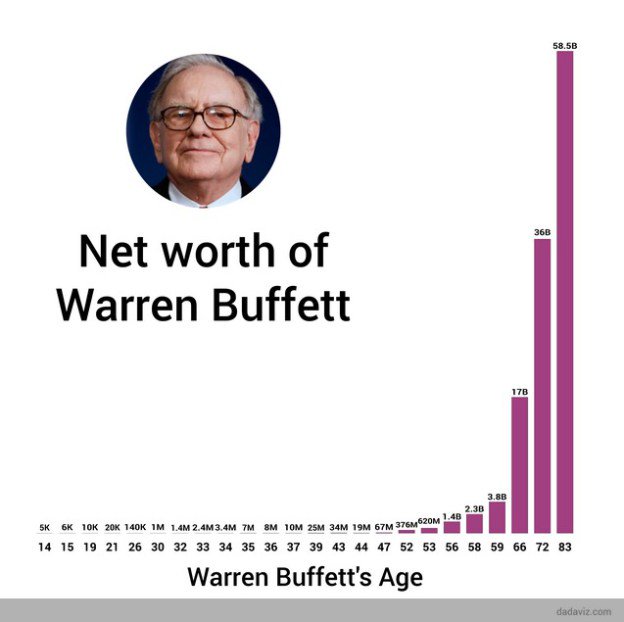

The Formula for Valuing All Assets

Using precise numbers is, in fact, foolish; working with a range of possibilities is the better approach.”

―Warren Buffett

https://hurricanecapital.wordpress.com/2016/12/02/the-formula-for-valuing-all-assets/

lundi 21 novembre 2016

warren buffet answer 20 questions

http://www.valuewalk.com/2016/11/warren-buffetts-meeting-university-maryland-mbams-students-november-18-2016/?all=1

interesting parts :

If you know who someone’s heroes are, then you will know how they will turn out

The most important skill in finance is salesmanship. That’s how you convince someone to marry you and that’s how you get a job. The most important quality to do well is temperament which would permit the control of fear and greed which have ruined many. Anyone who has become rich twice is dumb. Why would you risk what you need and have for what you don’t need? If you are already rich, there is no upside to taking on a lot more risk, but there is disgrace on the downside.

how to pick a friend:

Choose someone (among your friends and classmates) whom you would want 10% of their future earnings. Someone who is generous with a good sense of humor and you would want to be led by them.

dimanche 20 novembre 2016

samedi 19 novembre 2016

charlie munger & nassim taleb on doing what you love

"I've never taken notes. I never kept notes when I was a student. I just read what I please when I feel like reading it, and I think what I think when I feel like thinking it. And that's my system. I don't think it's the right system for everybody, but it seems to have worked well enough for me to enable me to get by."

- charlie munger

“The minute I was bored with a book or a subject I moved to another one, instead of giving up on reading altogether - when you are limited to the school material and you get bored, you have a tendency to give up and do nothing or play hooky out of discouragement.

- charlie munger

“The minute I was bored with a book or a subject I moved to another one, instead of giving up on reading altogether - when you are limited to the school material and you get bored, you have a tendency to give up and do nothing or play hooky out of discouragement.

The trick is to be bored with a specific book, rather than with the act of reading. So the number of the pages absorbed could grow faster than otherwise. And you find gold, so to speak, effortlessly, just as in rational but undirected trial-and-error-based research. It is exactly like options, trial and error, not getting stuck, bifurcating when necessary but keeping a sense of broad freedom and opportunism.

Trial and error is freedom.”

-Nassim taleb

lundi 14 novembre 2016

mardi 8 novembre 2016

lundi 24 octobre 2016

Tim cook = steve ballmer

https://steveblank.com/2016/10/24/why-tim-cook-is-steve-ballmer-and-why-he-still-has-his-job-at-apple/

they kill trial & error = no creativity

they kill trial & error = no creativity

mercredi 19 octobre 2016

.jpg)

mercredi 12 octobre 2016

Son on iot & buying arm

lundi 3 octobre 2016

jeudi 8 septembre 2016

dimanche 4 septembre 2016

mardi 30 août 2016

THe secret to Pe return

The secret to P/E return pays less then 7X on small cap

http://www.forbes.com/sites/danielfisher/2016/08/29/young-hedge-fund-manager-cracks-the-private-equity-code-small-stocks-and-leverage/3/#380c87db888f

http://www.forbes.com/sites/danielfisher/2016/08/29/young-hedge-fund-manager-cracks-the-private-equity-code-small-stocks-and-leverage/3/#380c87db888f

dimanche 28 août 2016

lundi 22 août 2016

mercredi 6 juillet 2016

mardi 7 juin 2016

vendredi 3 juin 2016

mardi 31 mai 2016

vendredi 27 mai 2016

Another great Howard marks memo

https://www.oaktreecapital.com/docs/default-source/memos/economic-reality.pdf

jeudi 26 mai 2016

mercredi 25 mai 2016

Benjamin Graham letters to shareholder

http://www.rbcpa.com/benjamin_graham/Graham-Newman_letters.html

samedi 21 mai 2016

vendredi 20 mai 2016

vendredi 6 mai 2016

jeudi 5 mai 2016

mardi 19 avril 2016

the world will only get weirder, the downside of rules

http://stevecoast.com/2015/03/27/the-world-will-only-get-weirder/

ask the 5 why's

rules can cover 80% of case but not tail event thus we're left with tail event

ask the 5 why's

rules can cover 80% of case but not tail event thus we're left with tail event

lundi 11 avril 2016

samedi 2 avril 2016

vendredi 1 avril 2016

vendredi 18 mars 2016

mercredi 16 mars 2016

lundi 14 mars 2016

stock you should not own

http://osam.com/pdf/Commentary_StocksYouShouldntOwn_Jan-2016.pdf

outperforming by avoiding the low quality stuff

outperforming by avoiding the low quality stuff

jeudi 10 mars 2016

why low oil price are good for the american economy

https://www.scribd.com/fullscreen/301250188?access_key=key-BT8y8UPDxzfvJSRxIC7n&allow_share=true&escape=false&view_mode=scroll

warrend buffet interview page 8

the reason the pain is felt is that capital value disapear faster then the low price dividend

warrend buffet interview page 8

the reason the pain is felt is that capital value disapear faster then the low price dividend

we don't pay enough for tranportation

https://transportationist.org/2014/08/04/we-dont-pay-enough-for-transportation/

a good exemple of society at large failing to consider the opportunity cost

a good exemple of society at large failing to consider the opportunity cost

jeudi 25 février 2016

jeudi 18 février 2016

mercredi 17 février 2016

Elon Musk on Regulators

https://www.farnamstreetblog.com/2016/02/elon-musk-regulators/

There is a fundamental problem with regulators. If a regulator agrees to change a rule and something bad happens, they can easily lose their career. Whereas if they change a rule and something good happens, they don’t even get a reward. So, it’s very asymmetric. It’s then very easy to understand why regulators resist changing the rules. It’s because there’s a big punishment on one side and no reward on the other. How would any rational person behave in such a scenario?

As Keynes said: “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.”

There is a fundamental problem with regulators. If a regulator agrees to change a rule and something bad happens, they can easily lose their career. Whereas if they change a rule and something good happens, they don’t even get a reward. So, it’s very asymmetric. It’s then very easy to understand why regulators resist changing the rules. It’s because there’s a big punishment on one side and no reward on the other. How would any rational person behave in such a scenario?

As Keynes said: “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.”

mardi 16 février 2016

jeudi 11 février 2016

{kind=link}

jeudi 4 février 2016

lundi 1 février 2016

jeudi 28 janvier 2016

ackman on index funds

http://assets.pershingsquareholdings.com/2014/09/Pershing-Square-2015-Annual-Letter-PSH-January-26-2016.pdfbill ackman on index fund

The problem of asset flows without regard to valuation is compounded by the fact that the most popular indexes are market-cap weighted. This means that the larger the market cap of the company, the larger its representation in the index. In other words, as the stock price rises, its weighting in the index increases, and the index fund is required to buy more of the company. While value investors typically buy more as stock prices decline (assuming intrinsic value has also not declined), market-cap weighted index funds do the opposite. They are inherently momentum investors, forced to buy more as stock prices rise, magnifying the risk of overvaluation of the index components.

mercredi 20 janvier 2016

lundi 18 janvier 2016

vendredi 15 janvier 2016

howard mark memo : on the couch

https://www.oaktreecapital.com/docs/default-source/memos/on-the-couch.pdf

interesting facts

1)the effect of a slowdown in china is almost negligible to the us account for less then 1% of s&p 500 profit and export to china = less then 1% of gdp

2) the low oil price amount to the equivalent of a reduction in taxes of 100's of billions

fear of lower car sale due to higher interest when the cost to drive oil is going down are unwarranted

3) psychological contagion : last week most stock exchange we're down approximately 7% even if the global event should have totally different repercussion on them

interesting facts

1)the effect of a slowdown in china is almost negligible to the us account for less then 1% of s&p 500 profit and export to china = less then 1% of gdp

2) the low oil price amount to the equivalent of a reduction in taxes of 100's of billions

fear of lower car sale due to higher interest when the cost to drive oil is going down are unwarranted

3) psychological contagion : last week most stock exchange we're down approximately 7% even if the global event should have totally different repercussion on them

lundi 11 janvier 2016

the simplest definition of a moat

If your competitors know your secret and yet still can't copy it, that is a structural advantage.

The capitalism distribution

http://www.theivyportfolio.com/wp-content/uploads/2008/12/thecapitalismdistribution.pdf

Observations of individual common stock returns, 1983 - 2007

Observations of individual common stock returns, 1983 - 2007

mercredi 6 janvier 2016

Sanjay bakshi on buying and selling

http://www.fool.com/investing/general/2016/01/05/value-investing-genius-sanjay-bakshi-when-you-shou.aspx

mardi 5 janvier 2016

Edge org most important scientific discovery of 2015

http://edge.org/contributors/what-do-you-consider-the-most-interesting-recent-scientific-news-what-makes-it

interesting one on antibiotics : http://edge.org/response-detail/26701

& on mating : http://edge.org/response-detail/26747

interesting one on antibiotics : http://edge.org/response-detail/26701

& on mating : http://edge.org/response-detail/26747

vendredi 1 janvier 2016

Inscription à :

Commentaires (Atom)